Job growth across the U.S. remained modest as year-to-date growth trailed the same period in 2015. This combined with light growth in GDP caused the Fed to once again hold off on pushing its benchmark interest rates any higher.

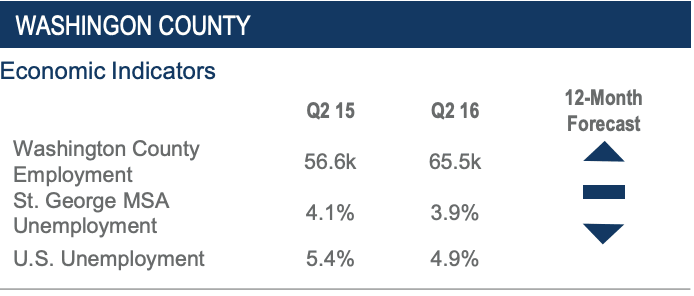

Utah added 44,400 net new jobs as job growth increased by 3.2% on a year-over-year basis.

Although the unemployment rate increased to 3.8%, this was not the result of weakening in the job market but rather wage growth that has pulled people back into the labor market that was previously sitting on the sidelines.

Office Market Overview

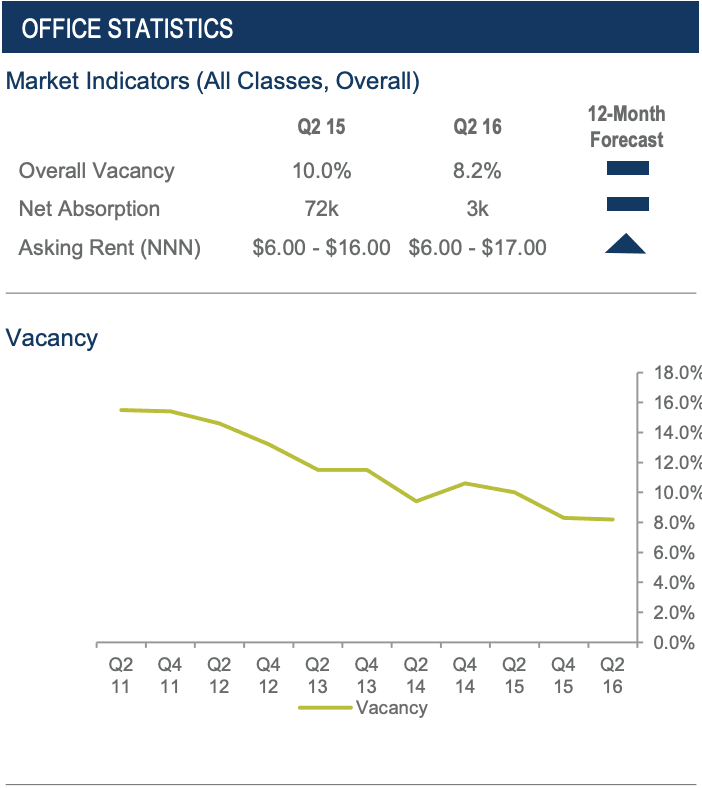

After finishing 2015 in strong form, the office market through the first half of 2016 continued to strengthen although a more modest pace.

Mid-year vacancy ticked down to 8.2%, which is the lowest the office vacancy rate in the past 9 years. Average asking lease rates held steady at $11.28 per square foot (psf) NNN equal to the year-end 2015 rates.

Net absorption was positive, but meager at 3,031 sq ft. There are no projects under construction, but there is 50,000 sq ft in the planning phase.

The prolonged recovery has caused a lack of viable spaces on the market for sale or lease. This is true particularly in the class A sector, where many of the remaining vacant spaces have asking rates and terms outside the parameters acceptable to most tenants.

This leasing grid-lock has frustrated both landlords and tenants to some degree, with some persistent vacancies from the landlord perspective and a lack of viable alternatives for tenants looking to expand or relocate.

The remaining vacant B and C spaces often have either, obsolete floor plans, location challenges, or older-building challenges, making them less desirable in the current market.

These factors will put increased pressure on rates as tenants compete for the best spaces and the best value offerings in the market in 2016.

Investment activity has slowed from the pace of 2015, but is still fairly active.

Industrial Market Overview

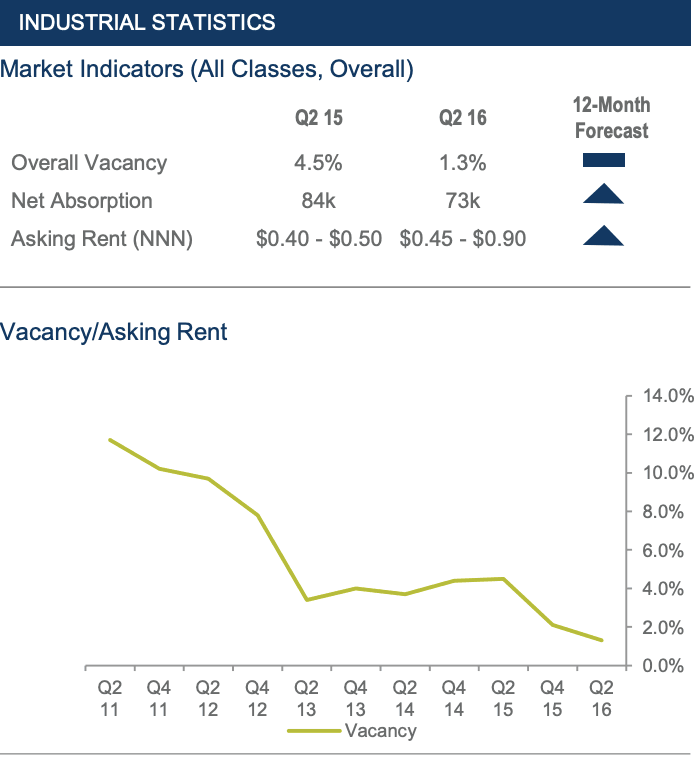

The industrial market reached an astounding historic low vacancy rate of just 1.3%. The industrial sector has shown strong gains in lease rates and per square pricing.

The lack of inventory has put a strain on the sector giving prospective tenants and buyers a few options to choose from.

Meanwhile, landlords and sellers have enjoyed a nearly 200-300% gain from the low point in the market both in average lease rates and per sf sale pricing gains, with a nearly 5-10% gain in the last 6 months.

Costs of construction have put a damper on new construction with

few spec buildings being added to the market—especially in the smaller to the medium-sized range.

Average lease rates have hit par with new construction on metal buildings with minimal buildout, and large industrial buildings. A gap still exists for other construction material types in the small to medium sector.

The largest contiguous space available in the market is 25,000 sf.

Retail Market Overview

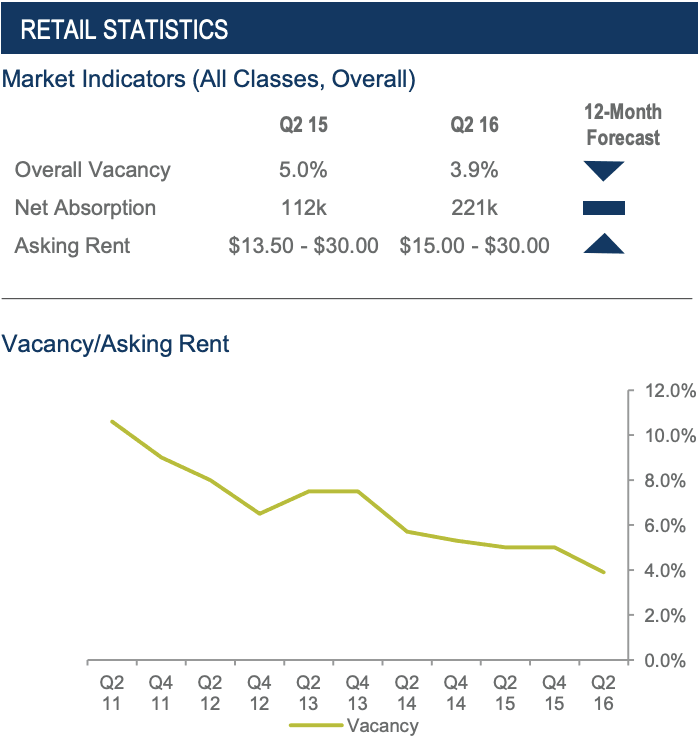

2016 has been a strong year for the retail market as vacancy continued to push lower. Several new buildings have been completed in 2016.

Retailers such as the 67,000 sf Harmon’s in Santa Clara and Lin’s Market in Washington Fields added much-needed grocery space.

Maverick opened a location on the corner of St. George Blvd. and 1000 East. Tagg-N-Go Car Wash opened its first location and has a second under construction.

Dairy Queen recently started construction as well and numerous other restaurants, financial institutions, and neighborhood service companies are also preparing to move forward on additional construction.

Stephen Wade’s new Mercedes Benz Dealership was completed in February. Holiday Inn Express next to the convention center opened this spring bringing 130 new hotel rooms to the area, along with its onsite restaurant Burger Theory.

Investment interest is very strong but there is very little product

being offered for sale. The Tonaquint Retail Building traded this

summer as did Aaron’s Rents.

From a tenant vacating space in the old St. George Industrial Park. Lease rates will continue to climb to meet new construction costs on masonry and concrete tilt-up buildings.

We will witness lease rates starting to bifurcate into different rates for office vs. warehouse, like what occurred in 2005- 2007, driven by new construction.

The best investment opportunities in this sector will be to pick up underpriced industrial land parcels, smaller single tenant buildings, or a larger spec building (50,000 SF +).

We expect lot sales and new construction to continue to increase at a measured pace as the leasing market adjusts to the new normal.

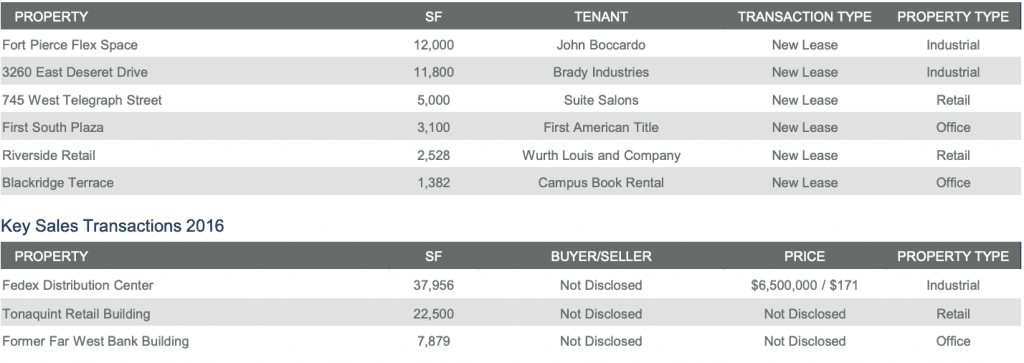

Key Lease Transactions 2016

Market Forecast

- Office vacancy is expected to decline as activity accelerates through year-end pushing lease rates upward by 5% or more.

- Supply constraints within the industrial market will continue into 2017 as new construction tries to keep up with demand. Lease rates are expected to continue climbing.

- New construction will continue as grocers, restaurants and other retailers continue to expand in the St. George market.

- Vacancy and lease rates for retail are expected to remain steady.

Travis Parry, SIOR, CCIM

Partner – LINX Commercial Real Estate

[email protected]

435-359-4901