St. George continues to draw accolades including Money Magazine’s 2015 “Best Places to Retire” for the great outdoors, drawing visitors, residents, and companies with its unsurpassed quality of life, warm climate, and outdoor activities.

Along with its business-friendly climate, this has helped push job growth to 2.2% over the last year, exceeding the national average of 1.9%.

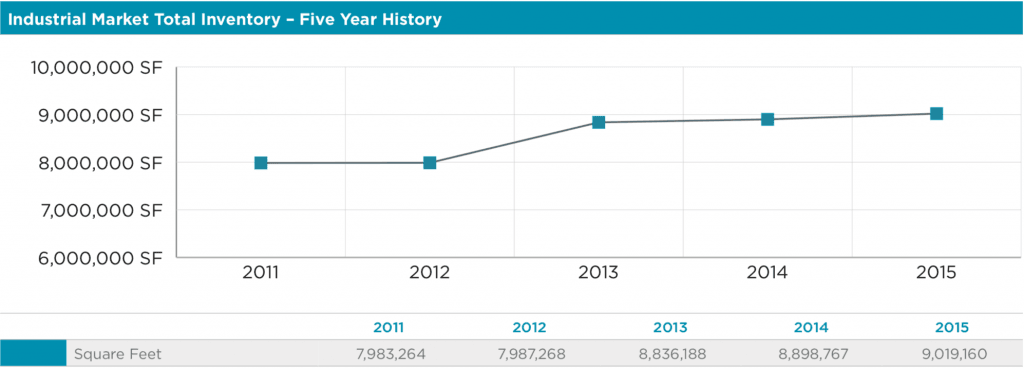

The appetite for quality real estate only continued to grow in 2015 as investors and owner-users continued to vie for quality assets.

The well-leased product continued to drive investment demand while owner-users were heavily focused on retail and industrial assets.

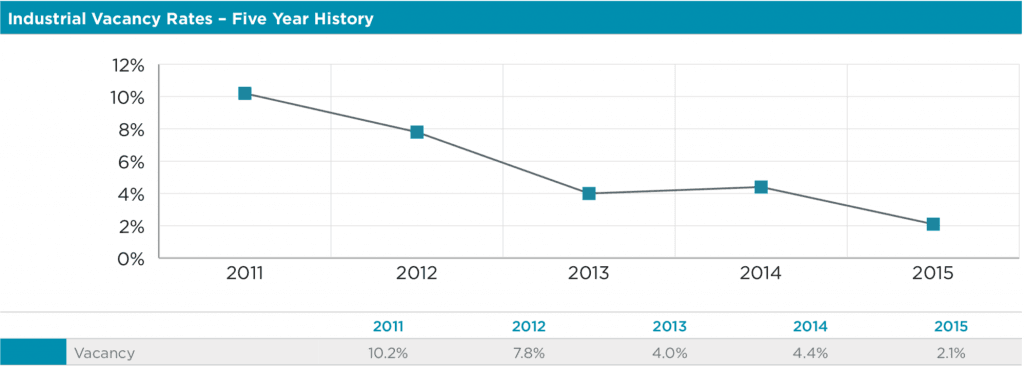

On the lease side, all sectors showed rental rate growth and reduced vacancy. Industrial vacancy saw the most significant change as over half of the available space in 2015 was removed from the market pushing the vacancy rate to just 2.1%.

Both retail and office saw healthy gains, as well as retail, dropped by 0.3 percentage points (pps) to 5.0% and office, dropped by 2.3 pps to 8.3%.

All three property types are currently at levels where finding space that meets tenants needs has become difficult.

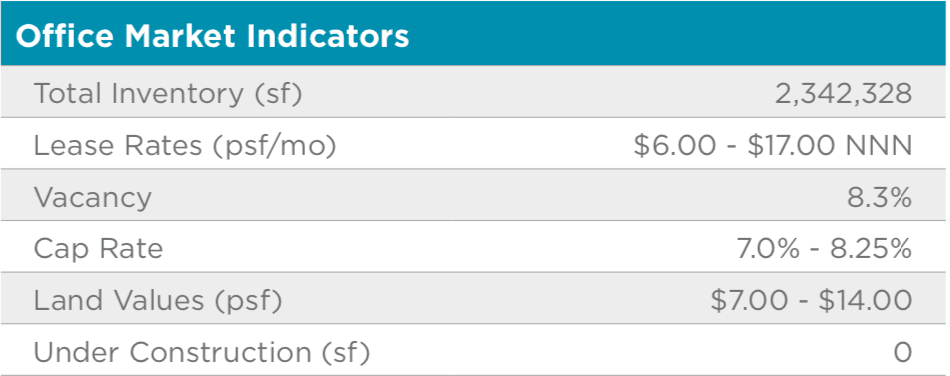

Office Market Trends

Office Market 2015 Year End Review

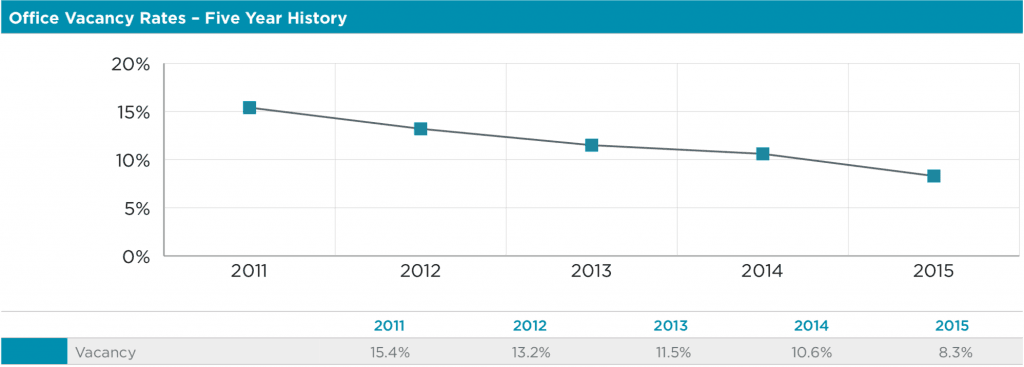

- Vacancy is down to 8.3% from 10.6% a year ago.

- Average asking lease rates (NNN) increased to $0.94 psf/mo from $0.88 psf/mo a year ago.

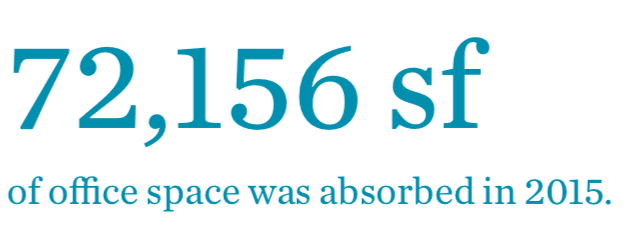

- 72,156 sf of office space was absorbed in 2015.

- 20,975 sf of new construction space added to the market.

The market showed steady improvement throughout the year, with year-end vacancy dropping below 8.5% for the first time since 2007.

Rates continued to increase and are expected to increase at a faster pace in 2016 due to limited space.

Average asking lease rates improved to $0.94 psf/mo NNN up from $0.88 psf/mo at year-end 2014. Absorption was steady with 72,156 sf of vacant space, equal to 3.1% of the total market, absorbed in 2015.

A 20,795 sf medical office building for Southern Utah Kidney represents the only new construction this year.

The long recovery has caused a lack of viable spaces on the market for sale or lease. This is true particularly in the class A sector, where many of the remaining vacant spaces have to ask rates and terms outside the parameters acceptable to most tenants.

This leasing grid-lock has frustrated both landlords and tenants to some degree, with some persistent vacancies from the landlord perspective and a lack of viable alternatives for tenants looking to expand or relocate.

The remaining vacant B and C spaces often have either, obsolete floor plans, location challenges, or older-building challenges, making them less desirable in the current market.

These factors will put increased pressure on rates as tenants compete for the best spaces and the best value offerings in the market in 2016.

Office Market Forecast

We expect the improving trend to accelerate in 2016, with vacancy decreasing and lease rates improving further. Lease rates should increase 10% or more by year-end 2016.

Investment activity has been fairly active, with a handful of investment sales taking place, primarily in class A buildings.

Tonaquint Building C is a notable building in that category that traded hands in 2015.

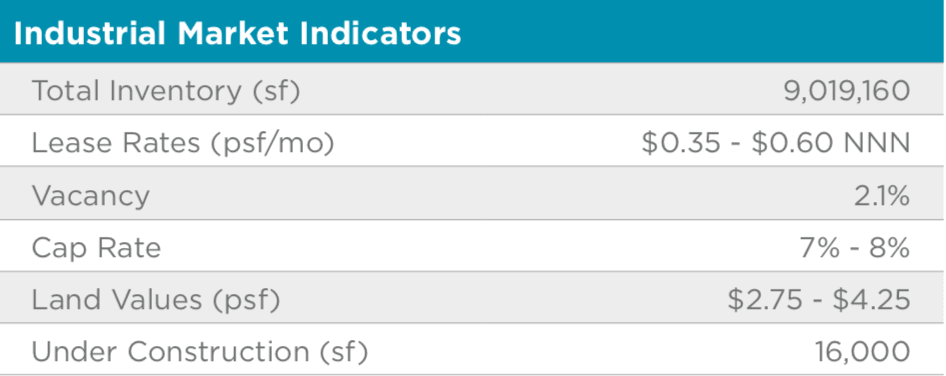

Industrial Market Trends

Industrial Market 2015 Year End Review

- Average asking lease rates (NNN) increased to $0.48 psf/mo, up 15% year-over-year.

- Extremely tight space market with vacancy coming in at just over 2%.

- Bulk of the vacancy exists in the mid-range multi-tenant space of 10,000-20,000 sf.

- Former 150,000 sf Blue Bunny production facility sold to Dean Foods.

- Little new construction on the immediate horizon combined with very low vacancy will create acute leasing conditions.

Average asking lease rates increased year-over-year.

The industrial market in Washington County dropped to a low vacancy of just over 2% – numbers we have not seen since the 2005 real estate boom. The sale of the 150,000 sf former Blue Bunny production plant accounted for over half of the vacancy reduction.

The industrial sector experienced strong activity across both leasing and sales. Developers have been hesitant to build any spec space as memories of the recession linger in their minds.

As a result, essentially no new space is hitting the market with only 16,000 sf under construction.

The lack of new construction coupled with an extremely tight vacancy rate has lead to increasing rental rates and an acute shortage of lease space and existing buildings for sale in the market.

Across the size spectrum, the smaller spaces (< 5,000 sf) have the lowest vacancy range, while the mid to larger spaces in the 10,000 – 20,000 sf range have the highest.

Just over 120,000 sf of new construction inventory was added to the market in 2015, nearly 65% of which was owner-occupied.

Industrial Market Forecast

A low vacancy rate combined with little new spec construction will lead to further increases in lease rates.

New construction is expected to take place as these lease rates rise above levels necessary to support new construction.

The best investment opportunities in this sector will be to pick up underpriced industrial land parcels in preparation for the growing new construction market, smaller single-tenant buildings, or a larger spec building (50,000 sf +).

Retail Market Trends

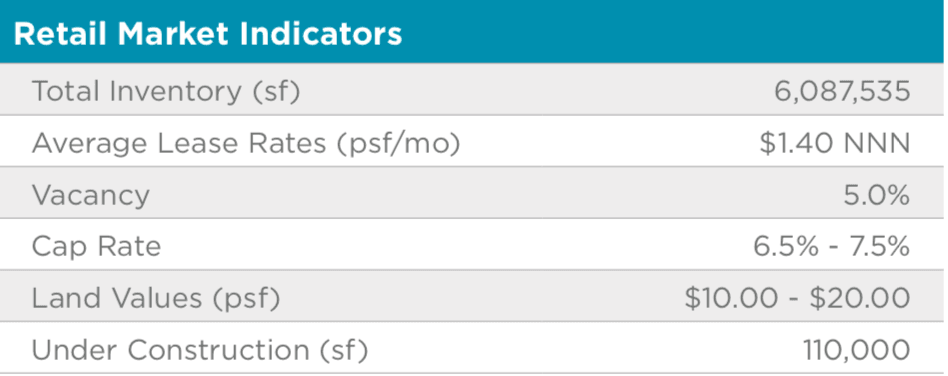

Retail Market 2015 Year End Review

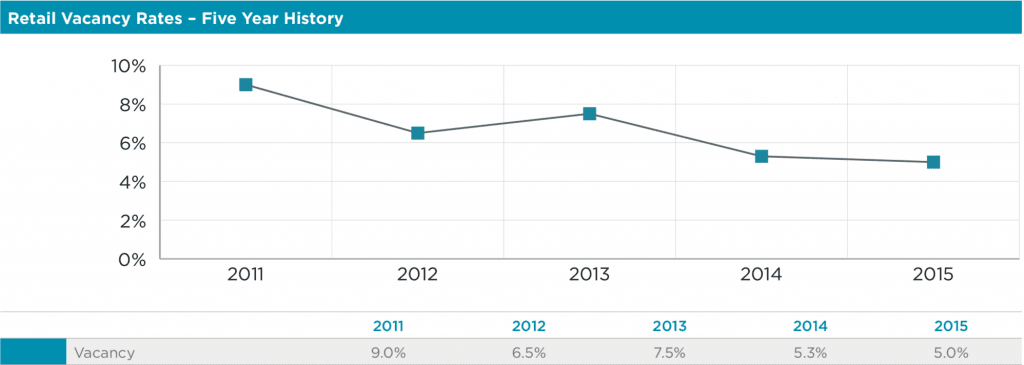

- Vacancy is down to 5.0%

- Average asking lease rates (NNN) increased to $1.40 psf/mo

- 99,000 sf of new construction space added to the market

- 110,000 sf currently under construction

- New grocery anchored centers have been the big news in retail this year

Investment interest remained very strong but with little product being offered for sale, investors fought over the few opportunities that were being offered.

The TJ Maxx anchored center and Rio Plaza center were the only notable retail center sales in the area.

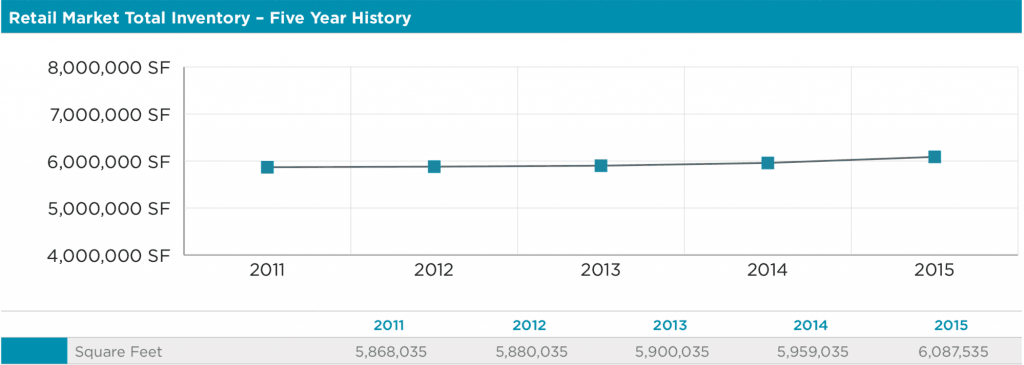

2015 was a strong year for the retail market. The vacancy is down to 5.0 % from 5.3% at year-end 2014.

New buildings in 2015 include

- Fiesta Fun’s addition of a 40,000 sf indoor facility that includes an arcade, bowling center, laser tag, restaurant and party rooms to compliment the entertainment park

- The Honda Polaris of St. George

- The Golden West Credit Union

- Tractor Supply and 2-Family Dollar stores in Ivins and Veyo

- Harmon’s newest location in Santa Clara is under construction and slated for completion in February 2016. The new 67,000 sf grocery store will service Santa Clara, Ivins, St. George and surrounding communities.

The new Lin’s Market is also under construction and currently on schedule to open the end of February.

The new location will bring much needed retail to the Washington Fields and Little Valley areas. Stephen Wade is bringing Mercedes Benz to Southern Utah – the new dealership is currently under construction on the corner of Black Ridge and Hilton drives.

Completion of the facility is scheduled in two phases with the first at the end of December 2015 and the second in the middle of February 2016.

The Hilltop Chevron, on the corner of St. George Blvd. & 1000 East, which has been a fixture of St. George for the last 45 years, was ground leased by Maverik.

Their new convenience store/gas station site is currently under construction and will be opening in February of 2016. Rumbi’s Island Grill and Chipotle restaurants both entered the Southern Utah market for the first time this year.

Holiday Inn Express has a new hotel underway, located next to the Dixie Center and in the final stages of construction.

Retail Market Forecast

We expect retail to attract significant attention next year with the completion of two new grocery-anchored centers around the corner.

This will bring new tenants and interest into the St. George market.

We expect that the vacancy rate will continue to decline, while lease rates continue to rise.

Travis Parry, SIOR, CCIM

Partner – LINX Commercial Real Estate

[email protected]

435-359-4901